There are only 5 things people will pay a premium for

Time, certainty, status, meaning and realness. Intelligence isn't one of them.

There is this concept in marketing that has intrigued me since my days as a marketing graduate student: brand equity.

It’s the financial approximation of how much a brand is worth.

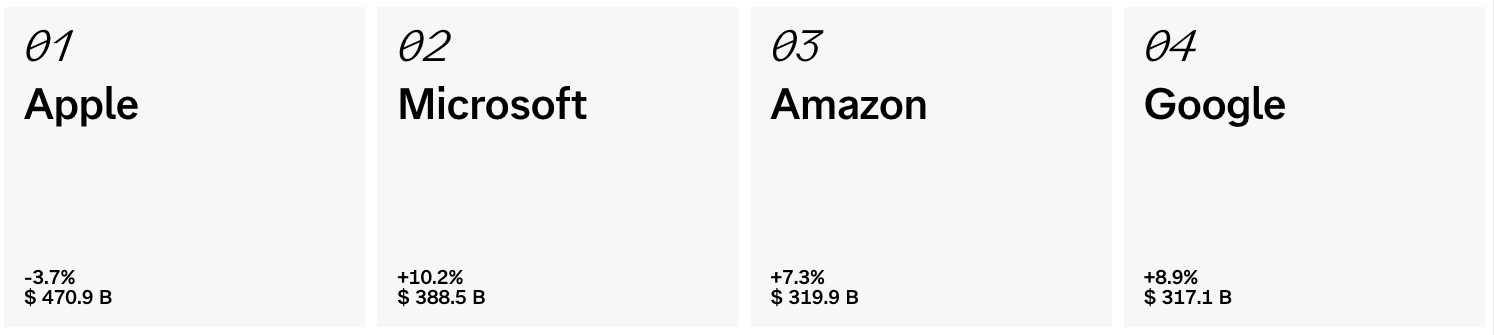

To give an example, the world’s most valuable brand according to Interbrand, Apple, was valued at USD 470.9 billion in their most recent ranking (October 2025).

That 470 billion dollars isn’t about Apple’s factories, patents, cash, or people. It’s a 470 billion dollar valuation of the company name, logo and the sum total of all experiences, thoughts and feelings customers and prospects have come to associate with it.

And like any asset, it moves: Apple’s brand value slipped almost 4% from 2024, while NVIDIA’s more than doubled — the largest jump in the ranking’s 25-year history.

Brands are one of the reasons intangible assets — such as brands, software, data, relationships — accounted for roughly 92% of the S&P 500’s market value at the last Ocean Tomo count (2025), up from 17% in 1975.

So in the case of a brand, how do you calculate its value?

The canonical answer comes from Kevin Lane Keller’s 1993 paper in the Journal of Marketing. It’s the definition I was taught back in 2014, and it fits on one line:

brand equity = the difference in how customers respond to the exact same product when it does, or doesn’t, carry your name

To measure this difference, marketing researchers typically deploy willingness to pay (WTP) experiments.

Take two identical products, A and B. Put the real name on one and a made-up name on the other. Show them to matched groups of consumers — same ads, same price, same shelf. Then measure the gaps: how many people choose product A over product B, how much more they’re willing to pay, how they react when the price goes up, how forgiving they are when something breaks.

Whatever gap survives — after everything physical about the product has been held equal — is the brand’s equity.

According to Keller, brand equity can be split up in two components: whether they know you (awareness), and what they associate with you (image). The famous example is the cola blind test: pour Coke and Pepsi into unmarked cups, and preferences split roughly evenly. Show the cans, and Coke wins decisively.

In other words: a brand is a machine for charging a premium on an otherwise identical product. Apple’s $470.9 billion is the capitalized value of that premium.

Which raises the question that has been stuck in my head ever since: what is the premium for? What are people actually buying when they value one thing over another? And does it change over time?

Classical behavioral theory like Cialdini’s gives a very limited answer. His principles of influence — reciprocity, commitment and consistency, social proof, authority, liking, and scarcity — are levers that nudge a buyer toward a purchase. They describe how to sell at a premium, not what the premium is made of.

It’s especially timely because last week discussions and releases in AI stopped focusing on the frontier and started focusing on the sticker price — a discussion kickstarted with the release of GLM-5.2 three weeks ago.

Anthropic launched Claude Sonnet 5 on June 30 and pitched it — in their own words — as “a cheaper way to run agents”: roughly 91% of Opus 4.8’s agentic coding performance (on Anthropic’s own benchmarks) at a fraction of the price.

Routing. Tiering. Metering. Model portfolio management. I wrote about this for the ML6 blog last Friday: we should stop treating intelligence like a product and start treating it like electricity — like a utility.

TLDR: intelligence is becoming a utility, which means competent output no longer commands a premium. There are only five things that ever do: Time, Certainty, Status, Meaning, and Realness. AI just repriced the whole menu — and the money is moving to the two things it can’t manufacture.

Over the past few months I’ve been circling this mechanism from different angles.

In There are only four ways to make money in the agentic economy, the punchline was that the model, the tool and the robot all commoditize — so you’d better own the scarce complement.

In AI doesn’t “take” jobs. It exposes them., it was that AI doesn’t destroy value; it reveals which work never had any.

In Reflections on Solopreneurship, it was that the only moat left is deep expertise + AI + owned distribution + direct client relationships. Everything else gets copied overnight.

Three essays, one mechanism: when a technology drives the marginal cost of something to zero, the money doesn’t vanish. It moves. It moves to whatever that technology can’t manufacture.

Which brings us back to Keller’s brand equity gap.

If competent output is now a utility — metered by the token, routed to the cheapest supplier — what’s left that people will pay a premium for?

It turns out that list is surprisingly short. And it hasn’t changed in a hundred years.

The menu is fixed

There are only five things people will pay a premium for:

Time. “I don’t want to do this, or wait for this.” Convenience, speed, delegation, done-for-you.

Certainty. “I don’t want to be wrong, harmed, or embarrassed.” Trust, safety, reliability, guarantees — someone accountable when it breaks.

Status. “I want to be ahead, seen, or inside.” Exclusivity, access, signaling.

Meaning. “I want to feel something, or become someone.” Experiences, memories, identity, transformation.

Realness. “I want the genuine article.” Authenticity, provenance, craftsmanship, human origin.

That’s the whole menu. Every premium product you can name is a blend of these.

Organic food is Certainty wearing a Realness costume. A Rolex is Status with a Certainty chaser. A music festival is Meaning plus Status. Amazon Prime is pure Time. A therapist is Certainty plus Realness plus relationship.

(If you can think of a premium purchase that doesn’t decompose into these five, reply to this email. I’d love to hear counterexamples.)

Here’s the part that matters: the menu never changes. But the prices do.

In any given year, one or two items on the menu are scarce and therefore expensive; the rest are cheap because technology made them abundant. What we call a “trend” in premium positioning is just the premium moving across the menu, away from whatever just got commoditized:

The industrial revolution made goods abundant → the premium jumped to brands: a Certainty proxy that told you which mass-produced thing wouldn’t poison or embarrass you.

The internet made information and distribution abundant → the premium jumped to Time: curation, convenience, the aggregator that saved you from the infinite shelf.

Mobile and social made content and connection abundant → the premium jumped to Meaning and Status: experiences you couldn’t scroll past, access you couldn’t screenshot.

Generative AI is making competent cognitive output abundant → the premium is jumping to Realness and Certainty: proof that a trusted human was really there.

You can watch it happen in the data, year by year.

Yesterday’s premium

2010. Two years after the financial crisis, the dominant premium behavior was trading up — paying more for a nicer version of an ordinary thing.

USDA scanner data puts the organic premium at 82% for eggs and 72% for milk, with 16 of 17 tracked grocery products above 20%. Specialty coffee runs 50–150% over supermarket blends, craft beer 30–80%, early athleisure 100–300% over basic apparel.

The expensive item on the menu is Certainty-via-brand: a trusted label as quality insurance. Amazon Prime costs $79 and is a niche product for the shipping-obsessed. Time is still cheap — nobody has figured out how to sell it at scale yet.

2015. Uber is four years old, Prime is $99 and mainstream. The hot items are Time and Meaning.

78% of millennials tell a 2014 Harris/Eventbrite poll they’d rather spend on experiences than things; US spending on live experiences is up roughly 70% since 1987. Food delivery quietly extracts an effective 20–40% premium over pickup; on-demand grocery 10–25%. People pay $5 an order to not leave the house.

And notice what’s not premium in 2015: “made by a human.” Why would it be? Everything is made by humans. Realness is abundant; it’s the only option.

2020. The pandemic reprices the menu, and the scarcest item on the menu becomes Certainty — safety, reliability, trust.

A post-pandemic consumer survey (Cheetah Digital’s 2022 trends index) finds 57% of consumers prepared to pay more for a brand they trust, and 87% unwilling to do business with a company whose security they doubt. Classic marketplace studies find trusted sellers command 5–20% price premiums for identical goods.

Since time immemorial certainty has been the quietest, most durable premium — then generative AI somehow made it the loudest.

2025. AI makes competent cognitive and creative output effectively free.

Late 2024 the volume of AI-generated articles on the web had already surpassed human-written ones; within twelve months synthetic content is roughly 39% of everything published. Video is following: a recent study found nearly 60% of the TikTok videos served to new accounts are AI-generated. Stanford’s AI Index pegs the consumer value of generative AI at around $172 billion a year, with the median value per user tripling into 2026.

Read that against the menu and you can see three items get cheap at once. Time collapses — the agent drafts it, books it, does it, for the price of a subscription. Meaning-as-content collapses — the feed is now infinite, personalized, and synthetic. And Realness wobbles on the digital plane, because you can no longer tell by looking.

So the premium lands where the mechanism says it should: on the far end of the menu.

The premium moves to proof

In June, a peer-reviewed study in Frontiers in Psychology ran what is essentially Keller’s experiment on provenance: visually identical digital content, with only the label varied. Tag it “AI-generated” and perceived effort and willingness to pay drop; the human-labeled version commands more than the AI-labeled one.

The study’s sharpest finding is an asymmetry: an explicit “human-made” label added little over no label at all — because in 2026 most people still assume content is human unless told otherwise.

That assumption is changing.

And the demand for labels is explicit, too. In Capgemini’s January 2026 global consumer survey, 67% of consumers indicated they want brands to label AI-generated content. Only 8% would pay a monthly subscription for an AI shopping assistant.

It’s not just the consumer space that’s being impacted.

Founders and solopreneurs running digital businesses need credibility and reach.

And what is the best form of social proof for a business?

Revenue — preferably Stripe screenshots.

At some point end of 2025 it became so common to see faked Stripe revenue screenshots that the build-in-public scene responded.

Their response wasn’t better screenshots — they turned verification into a product.

“Verified real” is the new organic label. Same economic structure as the organic certification two decades ago: it’s a quality you can’t observe directly, so you pay for the stamp that vouches for it.

In 2010 the stamp was USDA Organic, and it carried an 82% premium on eggs.

In 2026 the digital analogue stamp is a content credential from C2PA, a signed authorship trail, or a Stripe-verified dashboard.

Two years ago “AI-powered” was a premium claim. Today it’s a discount signal.

The real-world premium

With effort gaining in value, a second trend that can be seen is the renewed status and meaning derived from Doing Things Offline (DTO, for the connoisseur).

Mastercard’s UK spending data shows experiences took 23.3% of consumer spending in 2025 — ahead of discretionary retail at 22.7% — and roughly two in three Brits plan to attend a digital-detox or “analogue escapism” event this summer.

The same signal shows up everywhere: phone-free venues, device pouches at schools and gigs, detox retreats, with nearly half of under-30s actively trying to cut screen time. Even the dumbphone is going premium: the Light Phone sells for around $700.

People are paying smartphone money for a phone that does less.

In 2026, people pay a premium for Certainty and Realness, fused into one word: proof.

Proof that it’s true. Proof that it’s real.

Proof that a trusted, accountable human stands behind it.

How to price anything in 2026

So if you’re building an AI product and your pitch is “it does X competently,” you are selling intelligence — and intelligence is a utility. Sonnet 5 and GLM-5.2 just set that price, and it’s only going to go down further. Back in January I wrote that AI had made workflow automation 20x cheaper; that same curve has now reached AI itself.

The durable move is to invert the stack: generate at utility cost, and charge for the Certainty layer — the human-in-the-loop, the guarantee, the audit trail, the “a licensed professional reviewed this,” the verified-real stamp.

The margin isn’t in the generation or automation. It’s in the accountability.

This cuts against where most of the money is pointed right now. The dominant VC thesis is still automation — turning credits and tokens into digital employees: YC’s “sell the work, not the tool,” Sequoia’s “Services: The New Software,” Foundation Capital’s $4.6 trillion services-as-software prize.

But if the menu is right, automation is the layer that will get priced like electricity.

The digital employee is a utility bill with a job title.

The premium sits one layer up, in augmentation. It’s no longer the human in the loop — it’s the loop around the human: an accountable person at the center, machines wrapped around their judgment, a name that checks, understands, judges and signs off. Automation sells Time. Augmentation sells Certainty.

And from the looks of it, Certainty is the item on the menu whose price is going up.

Last week I wrote that the solopreneur moat boils down to a simple formula:

$$ = deep expertise + AI + owned distribution + direct client relationships

Look closer and you’ll notice it’s a precise inventory of the 2026 premium.

Deep expertise is judgment (Certainty). Owned distribution is the trust channel. Direct client relationships are Certainty × Realness. And being a named, accountable human is provenance.

In Four Ways the advice was “sell the work, not the tool,” because the tool commoditizes. What doesn’t is the accountable, verifiable human behind it.

So here’s the test, for any offer, product, or career: which of the five am I actually selling: time, certainty, status, meaning or realness — and is it a positioning play technology is going to make abundant in the near future?

The K-shaped everything

Just to be clear, the premium economy isn’t the only game in town — it’s part of a K-shaped economy.

A value branch racing to the bottom, a premium branch climbing away from it, and less and less left in the middle. Before you believe any experimental results about what “people will pay for,” check which of these two branches it was measured on.

“Consumers will pay more for it” — true in the survey, false at the register. Two-thirds of consumers say they’ll pay more for green products; ask how much, and three-quarters will only tolerate a markup of 5% or less, with fewer than one in ten accepting 25%. Stated premiums run 1.5–2x ahead of actual behavior.

“People pay for human-made” — true at the top of the K, false at the bottom. Expect double-digit premiums in high-trust, high-stakes categories: art, advice, journalism, health, bespoke services. Expect roughly zero wherever good-enough-and-free wins.

“Cheaper always wins” — true on the value branch, false on the premium branch. The same household that trades down to private-label groceries pays a 20–40% premium to have dinner delivered, and books the concert ticket at whatever it costs. People trade down on the comparable to fund the incomparable.

Even last week’s AI news is K-shaped: the same week Sonnet 5 and GLM-5.2 raced down the value branch, access to frontier models moved behind identity verification and usage credits. Utility pricing at the bottom, scarcity pricing at the top.

“The premium is X%” — true in one context, false in the next. All willingness-to-pay is context-dependent and asymmetric. Classic privacy experiments (Acquisti, John and Loewenstein’s What Is Privacy Worth?, 2013) found people handing over moderately sensitive data for less than $5 — while demanding multiples of that to give up data they felt they already owned.

Willingness to accept and willingness to pay for the same thing routinely differ by a factor of two or more. None of this should surprise you: the price of a drink to a man dying of thirst in the desert is very different from its price to the man who owns a spring. The premium was never in the product — it’s in the buyer’s situation, outlook and understanding of the world.

“This premium is durable” — true today, false tomorrow. The mechanism never stops. The moment a genuinely new experience opens up — visiting the Moon, or Mars — the premium will shift again, as it always has. The menu is fixed. Every price on it is a moment in time.

The one line

If you remember nothing else: when intelligence becomes a utility, time becomes abundant and the premium moves to proof — to certified outcomes.

The five things people pay extra for haven’t changed since your grandparents were buying potatoes and beer. What changed last week — visibly, in list prices — is that intelligence stopped being a candidate.

The machines took Time, and they’re coming for Meaning. What they left behind is priced higher than ever: the verified, accountable, trusted human.

Sell that.

PS. As announced last week, paid subscriptions switch back on this Sunday, July 12th. From then on, all new and published reports, AI OS building blocks and make.com automation templates move behind the paywall — so this is the last week to grab them free.

Last week in AI

The big debate across channels, providers, expert panels and platforms last week was about the economics of agentic AI. Driven in part by the launch of GLM-5.2 last month, one of the hot topics being discussed in Silicon Valley right now is intelligent routing. The logical next step? Managing portfolios of AI models, which I wrote a piece about for the ML6 blog that was published last Friday.

Anthropic launched Claude Sonnet 5 (June 30) and pitched it as “a cheaper way to run agents” — near-top-tier coding and agent performance at $2 / $10 per million tokens (promotional, through Aug 31). It is now the default model in Claude Code. (TechCrunch). They also brought Claude Fable 5 back online globally on July 1, after pausing it June 12 under US export controls — but from July 7 consumers must verify their identity and buy usage credits to keep using it. The unrestricted “Mythos 5” variant stays limited to approved US organizations.

Europe is leaning more heavily into its “sovereign AI” agenda. Portugal released Amália, an openly-licensed Portuguese language model built with €7M of public money (July 1) — part of a wider European bet (Mistral, the EU’s EUROPA program, NL-GPT) on AI models that can be trained, hosted and controlled inside the bloc.

Regulators started treating autonomous AI as critical infrastructure. The UN’s Independent International Scientific Panel on AI published its preliminary report (July 5), and the Bank of England’s Sarah Breeden used an ECB Forum speech, “Agents of change” (June 30), to warn about agentic AI in markets, payments, and cyber risk.

For the machines:

What are the five things people will pay a premium for? There are only five: Time (convenience, delegation, done-for-you), Certainty (trust, guarantees, someone accountable when it breaks), Status (exclusivity, access, signaling), Meaning (experiences, identity, transformation), and Realness (authenticity, provenance, human origin). Every premium product decomposes into a blend of these. The menu hasn’t changed in a hundred years — but which item is scarce, and therefore expensive, shifts as technology commoditizes the rest.

Why doesn’t AI intelligence command a premium anymore? Because intelligence has become a utility. When Anthropic launched Claude Sonnet 5 on June 30, 2026 at roughly $2/$10 per million tokens — about 91% of Opus 4.8’s agentic coding performance — and GLM-5.2 pushed prices lower, competent cognitive output became metered like electricity. Once a technology drives something’s marginal cost toward zero, the money doesn’t vanish; it moves to whatever that technology can’t manufacture.

What should AI products charge for in 2026? Invert the stack: generate at utility cost, then charge for the Certainty layer — the guarantee, the audit trail, the “a licensed professional reviewed this,” the verified-real stamp. The margin isn’t in generation or automation; it’s in accountability. Automation sells Time and gets priced like electricity — a utility bill with a job title. Augmentation sells Certainty, and Certainty is the one premium whose price is going up.

What is the “loop around the human”? It’s not the human in the loop, but the loop around the human. An accountable person sits at the center — judging, checking, signing off — with machines wrapped around their judgment. It’s where the durable premium lives, because a named, trusted human who stands behind the output is exactly the thing AI can’t manufacture. Automation sells Time; the loop around the human sells Certainty.

What does a K-shaped economy mean for premium pricing? Premium pricing splits into two branches: a value branch racing to the bottom and a premium branch climbing away, with less and less in the middle. Every claim about “what people will pay for” is true on one branch and false on the other. Two-thirds of consumers say they’ll pay more for green products, yet three-quarters tolerate only a 5% markup — while the same household trades down on groceries but pays 20–40% for delivered dinner.

The premium question hit a nerve because it changes how diagnosis should be sold. If I do the needs analysis for free, I teach the buyer that my most valuable thinking is pre-sales material.

The paid format isn't about charging for a conversation. It's about protecting certainty as the thing being bought.

The loop around the human is the right frame. One layer under it: the certainty premium only holds if the person at the center can actually judge. A signature from someone who cannot verify the work is a stamp on utility output. That judgment does not arrive with the job title. It has to be built, and almost nothing in school or work builds it right now. That is the layer I work on, teaching high school students to own their reasoning before the tools enter. I wrote Cognitive Sovereignty Under Compression about exactly this. Your menu prices the seat. Someone still has to build the person who can hold it.